How Trump Caused Inflation

Trump Blocked Regulations Against Price Manipulation; Biden Has Yet to Acknowledge the Problem

It was just one loophole. But it was big enough to swallow the global economy.

Wall Street created the loophole almost a decade ago, to escape U.S. regulation of complex financial trades related to commodities like oil and wheat. Then the Trump administration fortified the loophole.

On Tuesday, gas prices hit a record high. Today, the March Consumer Price Index is expected to show overall inflation still running above eight percent.

Republicans are blaming inflation on Pres. Joe Biden and rising wages. Democrats blame corporate price-gougers and Russian Pres. Vladimir Putin. There’s some truth in there: the war in Ukraine and pandemic-related supply-chain issues obviously caused price fluctuations.

But the massive, wholesale run-up of global commodity prices is out of step with the fundamentals of supply and demand, a growing number of analysts say. And functioning futures markets would be buffering against the volatility we’re seeing – and the inflation resulting from it.

In other words, if Putin throws a stone into the oil markets, well-regulated futures markets should smooth it out to a ripple. In a dysfunctional market, Wall Street blows it up into a tsunami. That’s why consumers are now underwater from rising prices on everything from gas to food to the rare minerals in their electronics.

On March 24, Public Citizen Energy Program Director Tyson Slocum wrote that, “The past two years have seen an extraordinary surge in commodities market volatility.” He cites “evidence of excessive [Wall Street] speculation.”

As Antonia Juhasz reported for The Guardian, oil supplies are actually at record highs, and so is trading. And, as Juhasz notes, industry analyst Phil Verleger has said shifts in fundamentals that once might have accounted for changes of a dollar or less per barrel are now leading to spikes of as much as $10 per barrel.

What isn’t widely understood is that this Wall Street speculation didn’t just happen. As regulators began crafting new rules based on the 2010 Dodd-Frank Wall Street Reform Act, Wall Street swung into action, sleuthing out loopholes they could use to smuggle their swaps and derivatives business out of regulatory jurisdictions. They succeeded.

Their solution was so obscure, however, that even Slocum hadn’t heard of it. When I explain how it worked, he says, “Well, that’s interesting…what you’ve just described to me, that seems to be a serious problem.”

That’s what regulators under Pres. Barack Obama thought, too, when they found out about it. But one month after they proposed a rule to fix it, Trump won the presidency. His appointees blocked the fix, and there’s no indication that the Biden White House is even aware of the problem (even though the Obama administration was).

That’s inflation’s dirty little secret in a nutshell. Here’s the nuts and bolts, and how Democrats can fix it.

Footnote 563

Dodd-Frank was supposed to clean up after the last Wall Street assault on the global economy, and prevent the next one. Then it was up to agencies like the Commodity Futures Trading Commission (CFTC) to translate Dodd-Frank into functional rules by which Wall Street and its regulators would operate.

An early draft of one CFTC rule focused on international swaps trades.

Unlike futures contracts, which are ostensibly just promises to buy or sell commodities at a later date, swaps aren’t traded on one of the big commodity exchanges. Swaps are one-to-one deals. Almost all of them involve a big Wall Street or private-equity firm. And they’re essentially bets on commodity prices. (Derivatives, including swaps, are financial instruments that derive their value from something else, in this case, the price of oil or beef or coffee or…)

It’s hard to understand the importance of swaps without recognizing that almost no one trading them is actually drilling for oil or slopping Berkshire swine. Something like 90 percent of these trades are done by financial firms, which means it’s Wall Street trades — not the tiny handful of trades still made by actual hog farmers or nickel miners — that dominate the market and, therefore, drive the prices. (If you can follow the jargon, check out what Wall Street did with nickel in March).

In the case of commodity swaps, the CFTC knew that other countries had virtually nothing like Dodd-Frank. Which meant Wall Street could escape CFTC regulation of its swaps simply by trading them via overseas affiliates.

Obama had provoked an angry firestorm on the left when he put former Goldman Sachs partner Gary Gensler in charge of the CFTC. But Gensler knew how Wall Street worked.

Swaps had only been invented (beware financial inventions!) back in the 1980s. Some traders were wary of them. So in 1992, the International Swaps and Derivatives Association (ISDA) made it standard practice for U.S. firms’ affiliates to back their swaps with a written guarantee that the parent company would stand behind them. Swaps trades were now safe (for Wall Street, anyway) because Wall Street was guaranteeing its affiliates making the swaps.

Gensler knew all this. And he knew the banks would use affiliates outside the U.S. to escape federal regulation. So the CFTC asserted its jurisdiction not just over Wall Street, but over every swaps trade carried out by any affiliate on the planet that was guaranteed by Wall Street. Can you see where this is going?

In an extraordinary 2015 Reuters investigation, reporter Charles Levinson revealed the inside story of how Wall Street found their loophole.

Edward Rosen was a derivatives lawyer with Cleary Gottlieb Steen & Hamilton. The firm had been hired by a coalition of 13 global banks to thwart the CFTC’s global ambitions.

By 2012, Wall Street’s biggest firms had been using ISDA’s boilerplate swap-guarantee forms for 20 years. But early that year, with the CFTC circulating draft policy, Rosen raised a simple question on a call with his Wall Street clients. According to Levinson, Rosen said: “What happens if you just stop guaranteeing those transactions?” That, it turned out, was the hundred-trillion-dollar question.

Wall Street pushed for the CFTC’s new policy to cover only “explicit” guarantees. In other words, Wall Street could keep trading outside CFTC jurisdiction, as long as its swaps were traded by ostensibly non-U.S. affiliates that had been guaranteed not in writing but with a wink and a nod.

By March 2012, Goldman Sachs had taken Rosen’s question to heart. The firm told clients they had to sign off on Goldman moving its swaps to London, Singapore, or wherever Goldman wanted, whenever Goldman wanted. Who’s gonna argue with Goldman Sachs when all the other big firms are all pulling similar stunts?

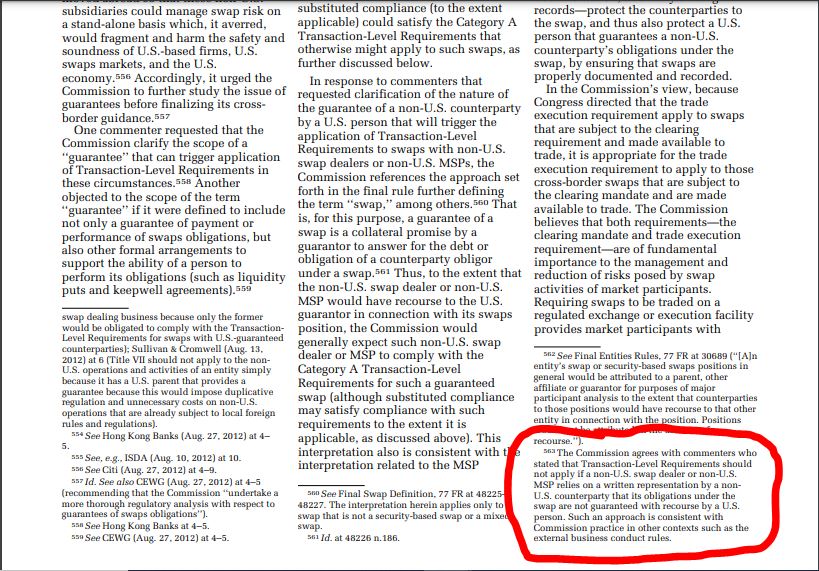

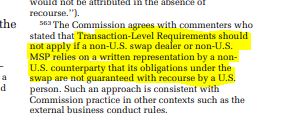

Gensler’s CFTC kept working on its new policy, unaware that Wall Street had already tunneled through it. On July 26, 2013, the CFTC finally issued its ”Guidance and Policy Statement.” And there, in footnote 563, the CFTC noted that its regulations wouldn’t apply if non-U.S. traders explicitly affirmed that they weren’t financially backed, or “guaranteed,” by a U.S. firm.

In other words, if a Spanish trader and a Hong Kong trader gave each other written assurances that they weren’t backed by Goldman Sachs or Morgan Stanley, then the CFTC had no jurisdiction. They could bet each other about oil prices all day long.

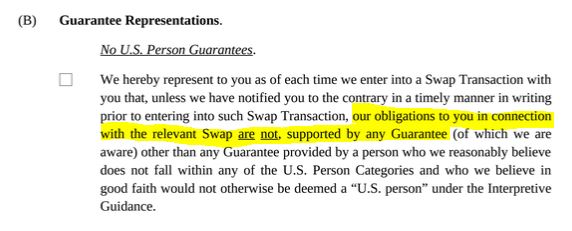

It took ISDA less than four weeks to formally, but secretly, invite all its members – the biggest financial firms in the world – to waltz right through the footnote 563 loophole. On Aug. 19, 2013, the ISDA sent its members a new form letter to use for their swaps. The form let traders affirm that no one in the U.S. was guaranteeing them simply by checking a box.

Technically, it was true – U.S. firms weren’t legally obligated to back up the swaps and other bets their affiliates made. But they risked reputational damage if they didn’t. And everyone knew it

(As Securities and Exchange Commission member Kara Stein explained just a year later, explicit guarantees weren’t needed anymore. The Wall Street Journal reported that in June 2014, Stein said, “The recent financial crisis is replete with examples of firms rescuing their affiliates… [and] firms do not jettison them off to fend for themselves in times of crisis; they bail them out.”)

Just one month after ISDA members got their new boilerplate forms for de-guaranteed swaps, Gensler spoke at the ISDA’s European Conference in London, on Sept. 19, 2013.

In his remarks, Gensler took a victory lap for closing an earlier loophole, which had let traders drive up gas prices to more than – wait for it – four dollars a gallon in 2008. Gensler told the conference attendees, the world’s top derivatives traders, “These reforms will finally close what had been known in the U.S. as the ‘Enron Loophole,’ which had allowed for unregistered, multilateral swaps trading platforms.”

Some of the traders there must have been laughing at Gensler. And even after politely listening to his demolition order for the Enron Loophole, none of them appear to have told him they had already set up camp in their new loophole, footnote 563, safe from the CFTC under the tent of the ISDA’s handy form letter.

While most companies who made stuff overseas wanted to slap “Made in the USA” on their products, Wall Street was now doing the opposite.

An American citizen who lived in Greenwich, CT, and worked for a U.S. firm, could now go to their office in lower Manhattan, arrange, negotiate, and execute swaps all day long, and keep them all from the CFTC just by checking a box “assigning” the swaps to a foreign affiliate. And on top of that, a good (or bad) number of these thousands of “non-U.S.” affiliates apparently were shells, legal fictions created on paper solely to conceal the fact that their products were secretly one of the few remaining things in the world actually manufactured entirely in the U.S.A. (The ISDA and the five financial firms mentioned in this report either did not respond to requests for comment or declined to comment.)

The Whistleblower

It’s not clear who snitched, but the CFTC found out about this in the spring of 2014. A 2018 paper published by the Institute for New Economic Thinking concluded it was “likely” that the CFTC got “tipped off.” The author of that paper was Michael Greenberger, who once ran the CFTC’s Division of Trading and Markets and then founded the University of Maryland Center for Health and Homeland Security, where he’s now the director. In a 2019 followup piece for the Journal of Business & Technology Law, Greenberger wrote that the tip-off came in May 2014. Greenberger told me he believes someone from ISDA “let the cat out of the bag.”

Either way, the CFTC was slow to respond. Greenberger wrote that the agency “at first unknowingly, and then largely unquestioningly” let Wall Street’s biggest firms keep moving swaps “overseas.” At the time, Greenberger writes, 90 percent of the swaps market was controlled by Citigroup, JPMorgan Chase, Goldman Sachs, and Bank of America.

The swaps exodus had already begun to attract the attention of business journalists. The Wall Street Journal’s Katy Burne reported in April 2014 that the four financial firms, plus Morgan Stanley, were “changing the terms” of their offshore swaps units, “so they don't get caught by U.S. regulations.”

By the time the CFTC got their tip, Gensler was gone. And it wasn’t until November 2014, Greenberger writes, that CFTC Chair Tim Massad first raised questions. The CFTC did manage to close the loophole for one type of Dodd-Frank swaps regulation. But 12 other types still had Wall Street welcome mats out.

In late 2016, the CFTC formally proposed new rules to close the footnote 563 loophole entirely. But by then it was October 18. The country was just three weeks away from President-elect Donald J. Trump.

Trump had come of age in Wall Street’s shadow, literally. His tawdry New York real-estate dealings played out in a world of mobsters, shady deals, and a steady stream of legal troubles and exposés. He was a fixture of lurid New York tabloid front pages while richer, respected, Wall Street titans appeared as line-drawn portraits in the Wall Street Journal.

Running for president, Trump pledged to do Wall Street’s bidding. His economic plan, he told Reuters in May 2016, would be “close to [a] dismantling of Dodd-Frank.” He wasn’t far off.

Enter Trump

The day Trump took office, CFTC member Chris Giancarlo took over as head of the CFTC. Giancarlo, a long-time veteran of the industry he was charged with regulating, had joined the CFTC under Obama.

It’s not that Obama chose Giancarlo for the job. But presidents can only appoint so many members of their own party to the CFTC. According to Eleanor Eagan of the Revolving Door Project, which tracks federal nominations, to appoint members of the opposite party, presidents traditionally defer to that party’s ranking senator. In Obama’s case, that was Sen. Mitch McConnell (R-KY).

Giancarlo would do McConnell proud. And he took Trump’s campaign promise seriously.

It wasn’t Trump’s fault (yet), but by February 2017, there was “massive… [swaps trading] misconduct” going undetected, former CFTC enforcement chief Aitan Goelman told Reuters. But Giancarlo wanted less regulation, not more. In March 2017, Giancarlo told the International Futures Industry Conference, “The American people have entrusted the Trump Administration to turn the tide of over-regulation.”

Giancarlo told his Boca Raton audience that the CFTC’s job was to help Wall Street, not restrain it. The CFTC, he said, had to “foster open, transparent, competitive and financially sound markets in ways that best foster American economic growth and prosperity.” At that point in Giancarlo’s prepared remarks, a footnote explains that, “The President’s executive orders… require elimination of two regulations for every new one issued.”

Meaning: No way in hell would Trump’s CFTC close the footnote 563 loophole. And that fall, Treasury Secretary Steven Mnuchin made it clear he wanted the footnote 563 loophole not only to stick around, but to take off its shoes and get comfortable.

An October 2017 Treasury Department report to Trump by Mnuchin and his counselor, Craig Phillips, refers to the then-still-pending CFTC rule that would close the loophole. Mnuchin and Phillips write that the CFTC should “reconsider” trying to regulate swaps between foreign U.S. affiliates “merely on the basis that U.S.-located personnel arrange, negotiate, or execute the swap.”

Mnuchin was explicitly telling Trump that the CFTC shouldn’t regulate ostensibly non-U.S. swaps merely because of the tiny, nitpicky fact that the swaps were actually done by U.S. traders for U.S. firms on U.S. soil.

By this time, footnote 563 had totally upended commodities trading. It wasn’t yet driving wild price fluctuations, but it was Hoovering swaps trades overseas and out of regulated territory.

By as early as August 2014, the volume of U.S. swap trades in regulated markets “had plummeted,” Levinson reported. By the spring of 2015, it was enough to shift the center of gravity. Levinson writes:

“This spring, traders and analysts working deep in the global swaps markets began picking up peculiar readings: Hundreds of billions of dollars of trades by U.S. banks had seemingly vanished.”

The trades were still happening, it turned out, but “the major banks had tweaked a few key words in swaps contracts and shifted some other trades to affiliates in London, where regulations are far more lenient.”

The shift, Levinson says, “reflected an effort by some of the largest U.S. banks – including Goldman Sachs, JPMorgan Chase, Citigroup, Bank of America, and Morgan Stanley – to get around new regulations on derivatives…”

By December 2014, Levinson reported, some swaps markets had lost 95 percent of their trading volume in less than two years.

In June 2018, Greenberger’s paper came out, connecting the dots. It reads like a detective novel, albeit one written for Wall Street nerds. Spoiler alert: Footnote 563 did it.

In the latter half of 2019, the CFTC got a new chair: Trump appointee Heath Tarbert. An industry attorney, Tarbert wasn’t just a former law clerk for Supreme Court Justice Clarence Thomas, his most recent gig had been as an acting undersecretary at the Treasury Department — working for Mnuchin. (Bloomberg later wrote that Tarbert had a “pared-back approach to policing overseas swaps trades.”)

Not surprisingly, by the end of 2019, Tarbert had made progress on Mnuchin’s earlier recommendation. Tarbert came up with a new rule correctly interpreting what Mnuchin meant by “reconsider”: Kill the 2016 proposal to close the footnote loophole. The now-Republican-run CFTC wrote:

“The Commission is today withdrawing the 2016 Proposal. …the Commission's current views on the matters addressed in the 2016 Proposal [have] evolved since the 2016 Proposal as a result of market and regulatory developments in the swap markets and in the interest of international comity…”

That last line about “international comity” alludes to European nations threatening a swaps trade war if the CFTC asserted international jurisdiction. (Never mind how much of the European swaps market was actually U.S. shell companies.)

The two Democrats on the CFTC dissented against withdrawing the rule. One of them, Rostin Behnam, wrote that Tarbert’s new rule was coming “seemingly in response” to Mnuchin’s recommendations, which, in turn, explicitly arose from Trump’s deregulatory executive order.

What About Inflation?

Greenberger’s 2018 paper was called “Too Big to Fail” because the concern was (and still is) that these commodity swaps could cause another crash a la 2008.

Without regulators checking that U.S. firms have the money to back up their bets, and with no transparency about who’s betting how much with whom, another global economic crisis is just one domino away. But a crash is just one peril of deregulating swaps.

If a global crash is the planet-destroying meteor of swaps, inflation is the global warming of swaps. And just as you can’t quantify how much of any given storm is caused by global warming, there’s no way to tease out the exact inflationary impact of swaps on any given commodity.

But in any industry, the pros can tell when the supply-and-demand fundamentals are out of whack with the market’s price-setting. That could mean price-gouging…but in that case, how come there’s no oil company hunting for market share by undercutting their price-gouging competitors? Those undercutters don’t exist, because everyone who actually sells real, black, gooey oil is outnumbered ten-to-one by traders who’ve never seen unrefined oil, let alone sold it.

“You can’t do it,” Greenberger says, referring to undercutting. “If somebody came to the market today and said, ‘I’m going to sell my oil at $80, it won’t work because of the futures/swaps price.”

So Wall Street dominates the swaps markets, which drive the futures markets (where Wall Street also bets), which drive the spot prices (ditto). Oil companies reap a benefit, for sure, but they couldn’t buck Wall Street if they wanted to.

But if Wall Street sets the price, why run it up? Because the bigger the bet, the more money they make.

If a Wall Street trader bets that oil will hit $80 a barrel, that bet influences how other traders bet. Someone’s likely to up the ante, even if it's just by a dollar. “It’s a self-fulfilling prophecy, so I win the bet,” Greenberger says. Left unchecked, it’s a one-way ratchet. “The prices are always going up until they’re finally caught.”

(As TYT reported at the start of the pandemic, those Wall Street firms secretly wanted to help oil-company clients by goosing the price of oil. How? By getting people back in offices – pre-vaccine, in the middle of a pandemic – so they’d have to buy gas to get to work.)

Greenberger told me that he was approached early this year by a Senate staffer who wanted to know whether Wall Street could be responsible for rising gas prices. Greenberger didn’t think so. After all, people were commuting and traveling again. The fundamentals of supply and demand lined up.

But by the time I spoke with Greenberger, with the same question the staffer had asked, prices had soared. And by then, Greenberger had changed his mind.

“We’ve got a war in Ukraine, but it doesn’t justify oil being at $100 [per barrel],” Greenberger says. And it’s not just oil. I ask him whether this dynamic applies to other commodities. He says, “Absolutely.”

According to Greenberger, “There is a question about how unmoored the [commodity] markets are from supply and demand,” but we can’t quantify it, because no one’s even investigating the possibility that it’s happening.

Why did I and a Senate staffer both turn to Greenberger on this question? Because he's the one who figured it out the last time Wall Street did this.

Biden’s Time

If you’re wondering why the CFTC hasn’t looked into this under Biden, you’re not alone. A CFTC source said that the CFTC can investigate fraud and manipulation, but looking into inflation is “not our remit.”

And for most of Biden’s presidency, the CFTC’s five-commissioner board hasn’t been at full strength. “The CFTC actually, this year, was without a quorum for a period,” says Eagan, who’s the research director for the Revolving Door Project’s governance team.

Biden could have had a Democrat-dominated board, as the law permits, after Tarbert left on March 5, 2021. But Biden didn’t send the Senate his first nominees until six months later, when the CFTC board was down to two commissioners.

“It took quite a while for Biden to nominate commissioners,” Eagan says. “Very often these nominations get overlooked, despite how important they are.”

She says, “The Senate moved a little bit faster in this case, but certainly not as quickly as one would have hoped.”

The Senate Agriculture Committee, which oversees the CFTC (because this used to be about farmers), sat on the nominations for months. The Senate confirmed Biden’s nominees more than a year after he took office.

Biden took “too long,” Slocum says. “And then the Senate [was] not acting fast enough.” Why the lack of urgency? Slocum says Biden “doesn’t have top people that understand commodity markets.” And Greenberger says, “there’s nobody on the Hill who’s really on top of this stuff.”

When Sen. Maj. Leader Chuck Schumer (D-NY) said last month that gas prices had Democrats “picking up the hood and shining a spotlight on how these corporations price and function,” he was referring to oil companies, not financial firms.

Whether the Biden CFTC will take any action remains unclear. The CFTC declined to comment and the White House did not immediately respond to my email. Slocum is clearly frustrated and tells me part of what motivated his March letter about excessive speculation was: “Where is the Biden administration there? Why do they continue to be silent?”

Slocum adds, “Biden has been committing a lot of unforced errors, but his mishandling of higher energy prices, I mean…I’m just at a loss.”

Biden’s CFTC chair is Behnam, the Democrat appointee who dissented back in 2019, so he would seem to be aware of the problem but might not recognize its possible ties to inflation. “We’ll see what Behnam is able to do,” says Slocum, who also sits on two CFTC advisory committees.

Either way, though, because Trump’s appointees killed the 2016 proposal, the CFTC would have to start new rule-making procedures from square one.

But the CFTC can take other steps. Greenberger told me the CFTC and the Dept. of Justice could launch antitrust investigations to root out any possible collusion by financial firms individually or via ISDA.

“A true antitrust enforcer would say ISDA is a charade,” Greenberger says. The question, he says, is “Does anybody at the CFTC care? …[N]o one who is a commissioner of the CFTC, at this point, has gotten into this deeply enough to understand that.”

And even just launching investigations could curb the kind of excessive speculation that supercharges prices, Greenberger says. “[I]nvestigations by federal agencies and Congress, in and of themselves, drive down excessive speculation and sky-high prices by big bank-driven speculation,” he says. “The banks run for cover with even a sustained whiff of regulatory — and perhaps criminal investigatory — seriousness.”

One remedy Greenberger offered in his papers came in the context of the Trump years – when federal action was unlikely – but it remains viable today. State attorneys general and other officials can file suit to enforce Dodd-Frank’s provisions. No one has done so, Greenberger says, because every agency has low-hanging fruit, far better understood, to pursue with their limited resources.

The irony is that Democrats, ostensibly the party of policy wonks, appear to have largely forgotten the lessons of the Dodd-Frank fight — or aren’t listening to its veterans.

Gensler and another Democratic CFTC alum, Dan Berkovitz, have their hands full at the Securities and Exchange Commission, a much larger agency. Others are in the private sector, getting paid by the industry they once regulated.

Two heavy hitters who understood the problem publicly supported Greenberger’s report back in 2018: FDIC Vice Chair Tom Hoenig and former Fed Chair Paul Volcker. But those voices are no longer being heard. Hoenig has retired. Volcker died one year after backing Greenberger’s warning.

Jonathan Larsen is TYT’s managing editor. You can find him on Twitter @JTLarsen.